Explaining ~100x revenue multiples for fintech companies using systems theory

We gaze with wonder at over $1 billion in raises announced last week, and over $10 billion in Fintech company value creation. Let’s look collectively at Checkout.com raising $450 million at a $15 billion valuation, Affirm more than doubling after its IPO to $30 billion, digital lending enabler Blend raising $300 million, and payments enabler Rapyd raising $300 million. As an adjacent API play, we can also mention MX getting $300 million as well for banking data aggregation.

What do all of these companies have in common?

Before we go there, however, we need some operating metrics. First up, Affirm with its $500MM+ in revenues and $4.6B of underwritten gross merchandise volume (total dollar amount of all transactions on the Affirm platform during the period, net of refunds).

We have discussed Affirm previously here, in particular highlighting the importance of Shopify and Peloton as key customers. The new information to add is that the company is now worth nearly $30 billion on the public markets, up from a bit over $2 billion in 2019. That is a good 60x multiple on top of a $110 million loss. Yes, never bet against the PayPal mafia, and Yes, the growth is phenomenal. And yet it is a 60x multiple on top of a $110 million loss.

In lending, we’ve also got Blend, which topped up $300 million. Blend is a “unified platform” for consumer lending, from mortgages to auto to credit cards and personal loans. It sits on top of the long tail of American banks and credit unions, and repackages the lending process to be automated to the reported tune of $3B per day.

What’s interesting here is that the platform is digitizing the store-front of the banks, and re-packaging into digital distribution. We don’t know for sure, but we suspect that the embedded API story will be one of the largest growth vectors in the future.

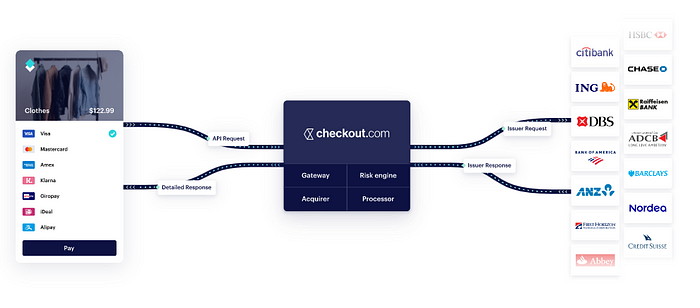

Then of course there is Checkout, with its $15 billion valuation and EBITDA profitability. Based on the linked article, we would guess that EBITDA is the $10–20MM range, printing maybe $50–100MM in revenue (Adyen comp), which is still a wild 100–300x on revenue.

For those of us that are not full-time payments analysts, it can be easy to get caught up in the difference between Checkout, Stripe, Adyen, and … what used to be Wirecard. We can tell that the company offers an all-in-one payments solution for merchants, and aggregates processing with acquiring, creating a bundle that is easy to purchase if you are a global retailer. The target market is upstream from Stripe, going after the larger commercial platforms which have international connectivity. There also appear to be pricing advantages to Checkout over Stripe, though it is hard to disambiguate.

This cross-border payments story is about two decades old, and we were surprised to see that Transferwise and Revolut are both Checkout customers. It explains a chunky part of Checkout’s valuation bump. The prior generation cross-border payments plays here, like Earthport and Payoneer, used very similar language and had a comparable value proposition. But they did not have the API-first design and the integration kits of these new players. Earthport exited to Visa for $230 million, and Payoneer quietly runs at $300 million in revenue. Traction in the old world is forgotten in favor of the hot new thing — integrating Alipay, ApplePay, and Klarna into eCommerce.

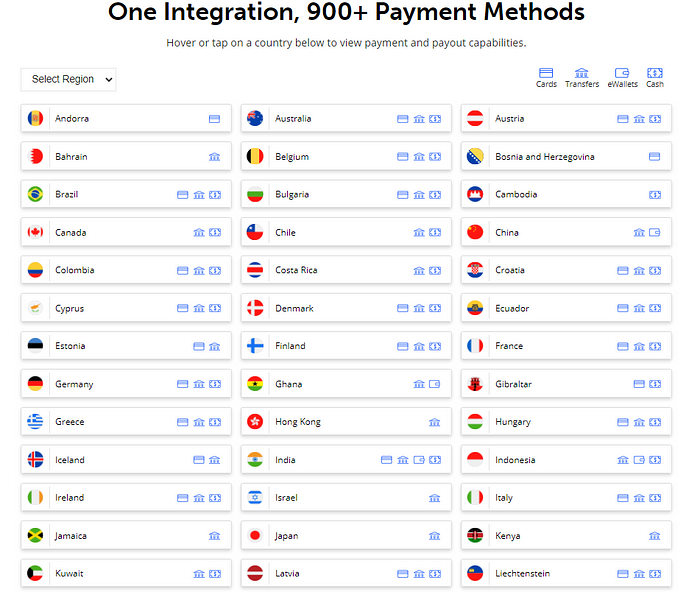

It is in this vein that Rapyd is competing for the very long tail of payment methods. Its $300 million raise is supporting wallets and accounts in over 100 countries and “900 payment methods”. The firm delivers an API payments product, and competes on reaching the last mile. It is comically comprehensive.

We understand it to sit *under* something like Checkout or Stripe, allowing for the flow and conversion of international moneys at scale. Perhaps even more importantly, it could sit under Google Pay or Apple Pay and reach into any country you like. Or alternately, under Paytm or Ant Financial. Thus the major option value of a globally connect payments network with regulatory approval.

Alright. This is enough evidence of 100x revenue multiple companies raising huge checks from Coatue and Tiger Management. Onto the mental model.

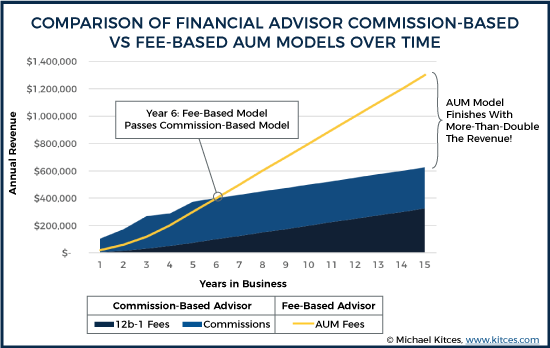

Stocks, Flows, and the Motion of Rents

In investment management, we used to call it transactional and fee-based revenue. Transactional revenue is what you would earn from trading as commissions. Fee-based revenue is what you would earn as a percentage from holding assets under management. Most financial advisors are switching to AUM based fees.

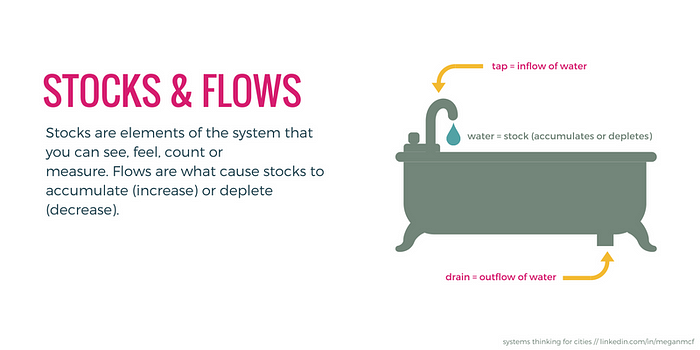

Alternately, you can think of it as stocks and flows. This is a systems-thinking framing. Some things accrue in a pile, and rise up to the sky. Or alternately, we dig holes in the ground and touch magma. These total levels are “stocks” and represent some accumulated amount of work over time, in the caloric sense.

Flows represent the change between stocks. You may have some amount of water here in reservoir A, and another amount of water here in reservoir B, and by opening up the dam, you create a flow of water from A to B at some rate of change. That rate of change is the derivative, or the velocity of the flow.

We are being imprecise, but that’s alright. As long as you get the sense of the difference between measuring *in place*, and measuring *the motion*.

And you can also extrapolate this thinking to say: reservoir A is some amount of USD, and reservoir B is some amount of Euro, and there is going to be some flow between the two. And the rate of change, and the supply and demand of each, will determine the flow. We call that the FX market.

Or alternately, there is some amount of USD, and some amount of toilet paper. And we call that the market for toilet paper. We measure the market of toiler paper by looking at total flow (excuse the potty humor, kids over the holidays, etc etc).

Ok! If we say there’s a stock of USD and a stock of companies that make paper products, and there is exchange between those asset types, we arrive at the brokerage market and at the market for equities enabled by exchanges. And the market for equities is similarly measured in the delta, in the notional volume of transactions, against which — you guessed it — brokers charge transactional revenue. Asset managers, on the other hand, charge against the pile of assets that includes the equity of this company.

Payments companies, especially those sitting on top of eCommerce trends, are taking a cut of (1) the growth of GDP, and (2) the secular growth of digital commerce vs. physical commerce. They clip a little coupon against a huge flow of digital transactions.

Banks, on the other hand, hold assets and take a share of the net interest margin, which is the arbitrage between sovereign interest rates and your puny human ones. This worked really well when there were such things as interest rates.

Let’s add one more tool to this toolbox. Lending businesses start out transactional, as they charge against each time they underwrite a loan. But they are also creating a negative stock, which is the liability of the unpaid loan. Their ability to accurately predict the risk that the liability hurts, and *match* that risk with the appropriate interest rate, is a key financial activity. Insurance is even weirder in that it creates an even bigger potential, but more unlikely liability, and it is this negative stock that yields a “fee-based” premium payment. Mortgages are similar in cash flow (periodic payment, negative balance sheet). Let’s understand that such complexity exists, but we don’t have to overanalyze structuring at this stage.

So the question with which we now sit is — where are the most profitable fintechs taking their economic rent? Where are they taking a slice of the pie? Is it better to take 3% against payments flow, or 0.50% against trading flow? Or, is it better to hold deposits and assets, and levy an annual fee against some cumulatively growing asset base? These dynamics are binary and quite different, creating entirely different incentives for the underlying firms.

- If you monetize against flow, then you want growth (positively said) or churn / overspending (negatively said). Schwab, Coinbase, and Robinhood are happy for you to trade 100 times a day, eroding capital gains to generate rents for the toll booth.

- If you monetize against assets, then you want to calcify and lock-in those asset forever, and trap your customers in an endless subscription cycle. BlackRock, Vanguard, KKR, and your monolithic 401-k providers want you to never check your account and put everything into a passive asset allocation. Set it and forget it, like a Netflix subscription.

- If you monetize against liabilities, then you want to take the transactional fee and pass on the underlying risk of non-payment or pre-payment to a capital provider. Ant Financial and SoFi don’t actually want to have you owe them anything, but they do enjoy some good debt origination. Lemonade is also in this bucket in re-financing most of its risks while collecting premia.

Transactional Models are Working

Venture investors, and public market investors attempting to mirror the narratives of venture investors, love revenue. Their love of revenue is matched only by their love of revenue growth. Traditional equity research analysts don’t love revenue nearly as much, knowing that it can be bought or grown unprofitably, without any return on equity. But if you are trying to land a big fintech exit, nothing says “winning” like a 30–100x revenue multiple.

Cost? Well, cost we can deal with “over time” and “after we scale”. Like WeWork.

Anyway, we don’t mean to be snippy, but a bit of rhetoric here and there can sharpen the mind. And in terms of revenue, it appears that in 2021 transactional businesses charging for change are putting up much more impressive numbers than fee-based businesses trying to prevent motion.

Affirm gets paid with every lending transaction in the eCommerce platforms that it powers. If its loans go bad, that won’t happen immediately, but over time. Blend indexes against digital distribution by banks, which is going to be slower but is still powerful when aggregated. Checkout gets paid with every transaction as part of its payment processing. Same for Rapyd, but at a lower level in the technology stack.

Money in motion rules the day in the public markets. But note that it is easier to generate transactional revenue against a flow, because the flow is endogenous. You need to take market share and be a participant, but you do not need to cause the flow. Monetizing stocks is harder, because you have to accrue them and cause your prospects to trust you over large periods of time with meaningful assets. However, such monetization is — at least in theory — much more sticky, and far more valuable on a per-dollar-in-revenue basis given a longer lifetime value of the customer.

So who is winning money at rest? Who is winning the fintech game of largest levels? We can point to Nubank and Tinkoff, or perhaps even Starling. But if we really want to see where money is coming to rest, look no further than Bitcoin and Ethereum. That’s a story for another time.

For more analysis parsing 12 frontier technology developments every week, a podcast conversation on operating fintechs, and novel food-for-thought essays, become a Blueprint member here.